Any government that does not control its money is controlled by those who do.

The Federal Reserve Monetary System

by Kevin McCormick, GPTX

The Federal Reserve was created in 1913, prior to World War I, in conjunction with the federal income tax. The income tax serves to circulate and redistribute money in the economy and to provide credibility for the federal debt, and the federal debt also supports the speculative financial markets, but that is another topic.

The key feature of the Federal Reserve Monetary System is that money takes the form of bank deposits which are created as loan proceeds. Nearly all money transactions are conducted through a "payment system" in which sums are subtracted from one bank account and added to another. In this way bank deposits fulfill the functions of money. In simple terms, a commercial bank makes a loan by adding the loan amount to the borrower’s bank (deposit) account. In practice, most loans require collateral, such as a house, automobile, or business asset as security for repayment of the loan. Often the loan proceeds are paid directly to the seller of the asset (to the seller’s account) and not actually added to the borrower’s account, such as in the “closing” of a house or auto purchase or a credit card sale. This deposit money did not exist before the loan was funded, so the commercial bank created the money through account entries. Thus, commercial banks control the creation, issuance, and use of new money.

The bank loan requires repayment of principal and interest. The principal payments reduce both bank assets and deposit balances. The interest payments also reduce deposit balances but are transferred to the bank’s account and spent by the bank. The money for the interest is not created in the initial loan process but instead must come from money created by other loans and circulated in the economy. However, other bank loans are not sufficient because they all suffer from the same limitation — not enough money is created to pay the principal plus interest on the loan.

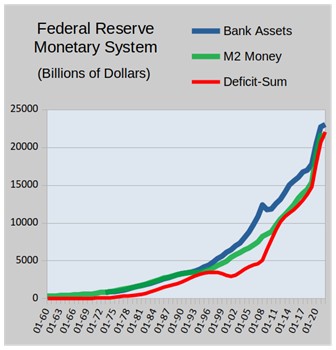

The accompanying chart suggests the source of the necessary additional money is the federal deficit. The federal government borrows money by issuing treasury debt and then spends that money into the economy through government payrolls, military spending, medicare, and other government programs. Since the deficit is borrowed, at least a portion can be newly created money from the commercial banks (facilitated by the Federal Reserve in secondary markets). Federal spending results in replenishing the private deposit accounts that have been reduced by loan payments, making the creation of new loans and deposits possible since the borrowers remain creditworthy. If the federal government balanced its budget and avoided a deficit there would be no money creation outside of the commercial bank and borrower network and many borrowers throughout the economy would be unable to make their loan payments, possibly resulting in a credit contraction and deflation. The federal debt compensates for the shortage of deposit money and allows monetary inflation through debt creation. Monetary inflation is often referred to as “economic growth” and is a constant fixation of corporate and political propaganda.

The chart shown uses data from the St. Louis Federal Reserve Bank. Note the close relationship between Commercial Bank assets (loans), the M2 money supply (deposits) and the accumulated federal deficits. The process begins with a commercial bank loan creating a deposit, then loan payments reduce the deposit account, and continues with the federal government borrowing and spending enough money to replenish the deposit balances counted in M2. The federal debt grows — with an ever increasing interest expense. To create money for interest payments the total debt must constantly increase. The chart shows the increase is approximately 7% compounded annually, which means the sums will double about every 10 or 11 years. The inflation is reflected in real estate and other asset prices, in increasing consumer prices, in the boom-bust credit cycle — basically wherever in the system conditions allow price increases.

The system is rather haphazard since there is usually no assurance that any given borrower will succeed in acquiring the money for debt payments. This is reflected in a competitive culture, pervasive economic insecurity, onerous debt obligations, great inequality, and periodic bailouts of privileged corporations.

In summary, commercial banks direct economic activity for their profits by creating loans and deposits. The deposits make up the money supply. The money supply is reduced by debt payments. The federal government issues treasury debt to borrow money that it spends into the economy, which maintains the money supply allowing borrowers to continue making payments and banks to create new loans and deposits, and thus inflate the monetary system. The income tax assures that interest on the federal debt will be paid. Needless to say, the federal debt itself will never be paid because to do so would deflate the monetary system.

This article has attempted to describe the basic design of the Federal Reserve Monetary System. As Michael Rowbothem states: this is a monetary system that actually operates in its own detached and limited mathematical world and which projects its own versions of the facts. The Grip of Death, A study of modern money, debt slavery, and destructive economics. Jon Carpenter Publishing, 1998.

Chart data references:

Board of Governors of the Federal Reserve System (US), Total Assets, All Commercial Banks [TLAACBM027NBOG], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/TLAACBM027NBOG, July 24, 2023.

Board of Governors of the Federal Reserve System (US), M2 [M2NS], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/M2NS, July 24, 2023.

U.S. Office of Management and Budget, Federal Surplus or Deficit [-] [FYFSD], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/FYFSD, July 24, 2023

The Vampire Banks are Sucking up All the Wealth

by Rita Jacobs, GPMI

Banks are cashing in on reliance on credit cards by squeezing out as much interest as possible.

They just can’t get enough. It’s like they’re on a campaign to see how much worse they can make it for everyone. When is enough enough? Wealth inequality is already at its highest level ever recorded in the US, and the banks want to make it even worse. There are no meaningful government policies to limit the sucking of wealth from the poor and middle classes in order to create the first trillionaire (if they don’t already exist). And goddess forbid that the government would do anything to make things better. The Federal Reserve System has been aptly described by some as a criminal banking cabal.

Besides inflation, falling wages, homelessness, high poverty levels, suicide rates, lack of mental health care, and crippling medical debt, we the people are now being subjected to crippling credit card interest rates. When people don’t have enough money to pay their ordinary expenses by living paycheck to paycheck, they often use plastic to get through the month. Bankruptcy rates per capita are 80 times what the rate was in 1920. How much worse can things get before people join together, rise up, and put a stop to this nonsense? Congress no longer cares about people, but passes laws that benefit the banksters every chance it has. And remember that bankers are also immune from criminal prosecution. How much worse can things get? Have we reached a point where phrases like “price control” and “interest rate control” been stricken from Congress’ vocabulary?

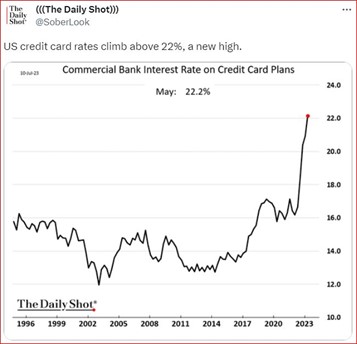

The statistics are in. Credit card debt in the US was just under $1 trillion at the end of the first quarter of 2023. The US Debt Clock shows credit card debt at $1.33 trillion in the second week of August. Obviously, people are increasing their debts in order to maintain their households. So, the banks have cashed in on this by raising the credit card interest rates. Here’s a graph that shows how credit card interest rates have been rising:

Who will be paying these high rates? Here is a chart that breaks down credit card debt by age group:

Source: Zippia.com

Bank-issued credit cards did not exist before 1958. By 1970 only about 15% of Americans had a credit card. Yet 28% of senior citizens 75 and over have the highest average amount of credit card debt. Older Americans are also the fastest-growing food insecure population in the US. The rising credit card debt, together with the jump in interest rates will create hardships on the already vulnerable members of society.

The overall average amount of credit debt is about $5,800 per person. If no additional debt is added, it would cost $160 per month over 5 years to pay off this debt — a total of $9,600, leaving the bank with $3,800 in interest income. The banks also profit by charging merchants fees for accepting credit cards from customers for payments. The average fee cost ranges from 2.25% – 2.50%. For credit card purchases totaling $5,800 the banks would extract an additional $137 from the merchants.

If you are not familiar with how money is created, you might think that banks are actually loaning money to their card holders that they have. However, the banks actually create new money when their customers use their credit cards. This adds money to that already in circulation. This is one way that banks create money in our debt-based monetary system. They have made no investment other than managing the system and billing to earn their profits.

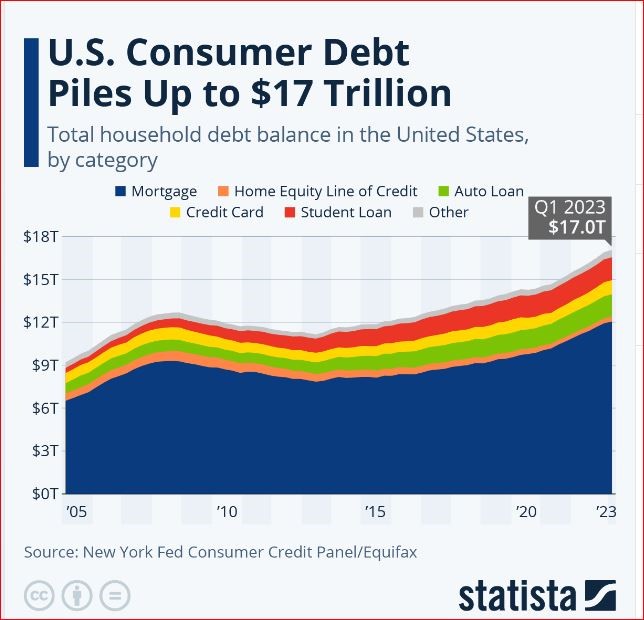

Here is a breakdown showing the rise of all types of consumer debt. It does not appear that this trend will reverse any time soon, since interest on nearly every type of consumer debt has risen since the Federal Reserve raised interest rates. Those who will profit the most from this rising debt are most likely already wealth. Surely Congress will do nothing to reverse this. Voting won’t change any of this either. If people do not rise up to protest this debt slavery, it will only continue to get worse.

Wall Street Greed Creating the Next Disaster

by Eugene Woloszyn, GPCT

After the bankruptcies & buyouts of the 2008 crash, 4 giant hogs dominate Wall Street:

JP Morgan Chase, with assets of $3.3 T

Bank of America, with assets of $2.5 T

Citibank, with assets of $1.7 T

Wells Fargo, with assets of $1.7 T

These 4 US banks have 40% of the assets of all 4,127 US banks.

Interest Rate Outrages

US banks now demand 7% home mortgages to customers with great credit scores. This is shattering the US housing market, particularly for first time home buyers. Hedge funds lick their chops waiting for the next crash to again buy large numbers of houses cheaply & turn them into rentals. Bank credit card divisions have increased interest rates from an already high over 17% to now over 22%. Home Depot & Amazon charge 30%. I recently received a credit card offer from one of the top 4 banks with multiple fees per month & a fine print compound interest of 36%. These rates are OUTRAGEOUS & way beyond the Federal Reserve Bank (FED) 5% interest rate increases in the last year & a half. This is an example of how corporations & executives decide how much to increase prices & interest rates on their products & services. Working people have no part of these decisions. Contrary to politician & media impressions, corporations create inflation & working people face the biggest impact.

Wall Street Crimes

The 4 largest US banks are frequently in the news facing customer class action law suits for shocking examples of bad business ethics, specialized fees & fine print betrayals of customer trust. These 4 banks end up paying settlements with the government in the billion dollar range. However, the FED enables giant banks to “admit no wrongdoing” & continue operations deducting their fines as a business expense on their taxes. This contrasts with the oil conglomerate Enron in 2002, which was forced to dissolve along with its national accounting firm Arther Anderson, & the stockholders were wiped out. But the FED has been bought by Wall Street. FED officials jump back & forth between Wall Street, the FED & corporate board seats. The first step in STOPPING WALL STREET DOMINATION OF THE GOVERNMENT IS BY ENDING THE FED.

Confidence in US banks as measured by Gallop has fallen from 60% in 1979 to 26% today. After the 2008 crash, which was primarily created by giant US banks, no US bank official went to jail, unlike those in Ireland & other nations. For documentation, see WallStreetOnParade.com which publishes a free daily report on bank crimes against the American people.

After the largest 4 banks, no other US bank is larger than US Bancorp with $540 Billion in assets. Even well know names are relatively small compared to the top 4. For example, Goldman Sachs with assets of $491 Billion, Capitol One $469 B, & Morgan Stanley $402 B.

Bank ownership in the US is tremendously concentrated. The top 100 US Banks have $19 Trillion in assets, but the top 5 have $10 Trillion in assets, or 52%. The bank regulator, the FED has effectively been captured by Wall Street.

In the last 16 years, the FED has approved 4,506 bank mergers and denied one.

2nd & 3rd largest US bank failures ever in Spring 2023

Silicon Valley Bank of California collapsed in Spring 2023, along with 3 other midrange banks with assets of $100-200 billion. Federal takeovers of these banks was required because they were insolvent. Depositor accounts were severely unprotected, because the Federal Deposit Insurance Corp (FDIC) only insures $250,000 per person or corporation in any individual US bank. The largest 10 accounts at Silicon Vallet Bank had an average of $3.3 BILLION on deposit in each account as their wheeler/dealer owners found it convenient to speculate on various investments.

Any reasonable working class person with this kind of money would subdivide it among hundreds or thousands of accounts at different banks to keep their money fully insured. The super rich are so arrogant that they can’t be bothered by these kinds of simple precautions. They also logically assume they will be BAILED OUT in any disaster as was done in 2008. BUSH II + OBAMA provided verbal sympathy, but practically no assistance as millions lost their jobs, savings & their homes foreclosed.

Silicon Valley Bank had 94% of depositor money uninsured. Two other insolvent & closed banks had 87% uninsured (Signature) & 67% (First Republic).

But these giant uninsured deposits also apply to our 4 giant US Banks:

JPMorgan Chase 52% uninsured, Bank of America 46%, Citibank 79%, & Wells Fargo 52%. These uninsured deposits are owned by bank customers who are very wealthy, are well connected with inside information, & will bolt the bank at the first sign of trouble. The Silicon Valley Bank Collapse saw $52 Billion in assets flee the bank electronically in one day. Foreign assets at US banks currently are not ensured. The FDIC seized all foreign deposits of Silicon Valley Bank. What would happen to the $1 Trillion in foreign deposits held in JP Morgan Chase & Citibank? An academic study has predicted that one of the 4 largest US banks could be at risk of a bank run. Giant US & world banks are “systemically risky” (in the words of the FED) & thus the FED is ready to bail them out in a crisis “or the entire economy will crash”. The American people must decide if they will again allow the FED + President + Congress of both major parties to scream “CONTAGION RISKS ARE REAL” (Fortune Magazine, 7-24-23). This is the war cry of the corporate lobbyists to justify massive corporate BAILOUTS. Note that conservatives are very opposed to further corporate bailouts. There is grounds for unity on this issue.

The super rich unprotected depositors of Silicon Valley Bank were BAILED OUT by the Biden Administration, although they denied it was a bailout. There are $7 trillion of uninsured bank accounts owned by 1% individuals & corporations in the US. This is 30% of the US GDP per year. Why should US Working people pay to protect the 1% who don’t want to subdivide their vast wealth into different banks with a maximum of $250,000 per bank?

STOP WELFARE FOR THE 1%.

UNINSURED DEPOSITS logically explain why banks do not use their assets to create bank loans. If banks tied up customer deposits in long term loans to businesses & home mortgages, they would be unable to stop bank runs like the $52 billion that fled Silicon Valley Bank in one day. Therefore, bank loans currently are NOT made from depositor accounts. Remember that 97% of dollars are electronic, with only 3% in coins or paper currency.

The Green Party Stand on this Bank Mess

The Green Party believes that new money is created, not by the FED or US Treasury, but by banks entering amounts ELECTRONICALLY in the accounts of borrowers & then charging years or decades of compound interest.

When US banks get scared like the present, when a recession/crash is near, the banks tighten their loan criteria, new loans (& thus new money) declines, & a recession/crash is made quicker & deeper. This power to create bank money & thus periodically crash the economy, must be ended. As Lincoln instituted with Greenbacks in the Civil War, we need non debt Sovereign Money & not be put in debt slavery by Wall Street. The unpassed NEED ACT of 2011 by US Representatives Dennis Kucinich & John Conyers would abolish the FED which has been captured by Wall Street & force Congress to do its Constitutional duty to “coin money & regulate the value”. These new improved Greenbacks must not be encumbered with bank debt, which is strangling the American people. Force banks to prudently create loans from depositor money & their own capital & stop the crazy speculation that crashes the economy.

Barbie; Warner Bros.

BARBIE and the Natural Economic Order

by Howard Switzer, GPTN

Creating an Egalitarian Society

I just read this great review by Ellie Griffin of the Barbie movie, (spoiler alert) as well as Charlotte Perkins Gilman’s 1915 utopian novel, Herland, and Taylor Swift's Eras Tour, well worth reading.

Herland describes a 2000-year-old isolated and prosperous civilization comprised entirely of women who lost all their men to an ancient war and began to reproduce via parthenogenesis (asexual reproduction). The result is an ideal social order, free of war, conflict, and domination. A society where motherhood is sacred, and everyone is either a mother or a mother to be and had great care of one another. A society where the children’s education was vital and integral to society. Their religion was Earth and life centered.

The Herland story begins with three men explorers who, having heard of a legendary society hidden deep in the mountains, set off in their airplane to go find it and did. They landed their plane in a remote area and set off to explore the society they had seen from above with beautiful fields, buildings, and roads with “fastmoving” (30 MPH) vehicles. Upon being discovered by the women the men were carried to a room where three women met them who interviewed them to learn who they were and all about where they came from as well as to tell them about who they were, their history and how the Herland society operated. The women regarded the men as an excellent opportunity to learn about a society that reproduced like the animals, whom they regarded with great love and care, it was an egalitarian sisterhood sharing power as none were advantaged over another.

Naturally the men tended to share only what they had assumed to be the positive aspects of their world but even then, the women of Herland were sometimes shocked by what they heard. The men realized that revealing the darker aspects of their society would be too traumatic for the women so did not. The three men had very different personalities but married the three women they had been partnered with who were contemplating the possibility that with men they could begin to reproduce like the animals did.

As an all-female society, they certainly embraced the Divine Feminine, the Great Mother Goddess, an architype that represents nurturing life which, in our patriarchal world, has been the subject of near continual repression for millennia. Herland was a conversational story describing the all-female society and contrasting it with our world that the three men explorers came from. Eventually, however, the men in Herland got homesick and left promising to never reveal the location of the hidden Herland allowing it to continue to flourish.

The movie Barbie was a story of self-discovery, self-reflection, exploration, and courage. It depicted a matriarchal society as well called Barbieland. In Barbieland, where every female was called Barbie, it was believed that Barbie dolls had liberated women in the real world. Unlike Herland there were men in Barbieland who all were called Ken. It was a peaceful society as well, rendered in a lot of pink plastic, and the Barbies oversaw everything. While Ken felt he had no value unless he had Barbie’s attention and, despite his disappointment, he accepted that “every night was girls’ night.”

Then Barbie, in the middle of a group celebration asks about death which brought everything to a halt. Barbie becomes dysfunctional and learns there is a rip in the membrane between the worlds. The wise “weird Barbie” told her, “to fix it you have to travel to the real world.” Ken went along. In the real-world Barbie discovers that women are not at all as liberated as she had believed and struggled with the cognitive dissonance she experienced. Ken on the other hand, discovered he liked the real world where he was shown respect and enjoyed privileges he had not experienced before, saying I feel “no undercurrent of violence.” Barbie, looking worried and stressed, says “that’s not what I’m feeling.”

Upon learning that a Barbie had entered the real world the board of directors of the toy company were in crisis. Having a Barbie in the real world would upset the patriarchy applecart. They set out to capture her and put her back in her box. Barbie escaped and fled with the help of a woman and her daughter and they all go back to Barbieland.

In the meantime Barbieland has been turned into Kendom. Ken has brought back the trappings of the ego-driven patriarchal world, mini-fridges full of beer, contact sports, flatscreen TVs etc. and considerable attitude. As the Kens play boy music, watch boy movies and be generally destructive and disrespectful. This creates an existential crisis in Barbieland.

The Barbies have a meeting to discuss what to do about it and come up with a plan to get the Kens fighting one another. This leads to an all-out war between two factions of Kens. Meanwhile the Barbies, taking advantage of the Ken’s inattentiveness, retake power in Barbieland and restore the Ken’s confidence in their ability to govern. The Barbies promise to appreciate and value the Kens. The trappings of patriarchy became unsatisfying to the Kens as the novelty wore off. Thus, peace and tranquility were restored, along with more equanimity, to Barbieland and we assume they lived happily ever after.

What does all this have to do with the Natural Economic Order? Well, Herland and Barbieland were both prosperous societies of economically independent women, and both had their own money systems, though this was not revealed in any detail. However, it reminded me of Silvio Gesell’s main work, The Natural Economic Order through Free Land and Free Money published in 1916, in which women were to be made economically independent of men. This was to be accomplished by making all the land publicly owned and leased to those who would make it productive while all the revenue would go to mothers. German economist and author Werner Onken explains:

LIKE THE SINGLE TAX REFORMERS of the Henry George School, Gesell held that the rental revenue from the land would enable the state to finance itself without the necessity of further taxes. In attempting to trace the rightful owners of these rental revenues in accordance with the principle of causality, Gesell concluded that the amount of rental revenue depends on the population density and this in turn depends on the willingness of women to bear and raise children. For this reason, Gesell proposed to distribute the revenues from the land rent in the form of monthly payments to compensate mothers for their work in rearing children. The maternal subsidy would vary in proportion to the number of their children under the age of majority. He advocated the extension of this scheme to include mothers of children born out of wedlock and foreign mothers living in Germany as well. His intention was that all mothers should be released from economic dependence upon working fathers and that the relationship between the sexes ought to be based on a love freed from considerations of power and economic dependency.”

So, Gesell, besides being an advocate for free land and free money also advocated free love!

Bernard Lietaer wrote in New Money for a New World that any society that worships an all-powerful male God is a patriarchy, and that, save mythical stories, there have been no matriarchal societies. This is because societies that believed in a female god were not matriarchal but rather were matrifocal and egalitarian, a sisterhood sharing power, worshiping the Great Mother Goddess, who represented the abundance of life and the ancient innovation of money. The shadow side of the Great Mother architype being greed and scarcity. Lietaer cited three occasions in history when such a system existed, Ancient Egypt, the High Middle-ages, and in Austria and Germany during the Great Depression.

Gesell’s “Free Money” was about eliminating the power aspect of money so that no one would be advantaged over another which was evident in the economies of both Herland and Barbieland. Gesell proposed money issued with a small monthly parking fee, called demurrage, required to maintain its face value. This fee eliminates the ability to accumulate and hoard money as well as eliminating its liquidity advantage over material goods. He wrote,

“Only money that goes out of date like a newspaper, rots like potatoes, rusts like iron, evaporates like ether, is capable of standing the test as an instrument for the exchange of potatoes, newspapers, iron and ether. For such money is not preferred to goods either by the purchaser or the seller. We then part with our goods for money only because we need the money as a means of exchange, not because we expect an advantage from possession of the money. So, we must make money worse as a commodity if we wish to make it better as a medium of exchange. So, we must make money worse as a commodity if we wish to make it better as a medium of exchange.”

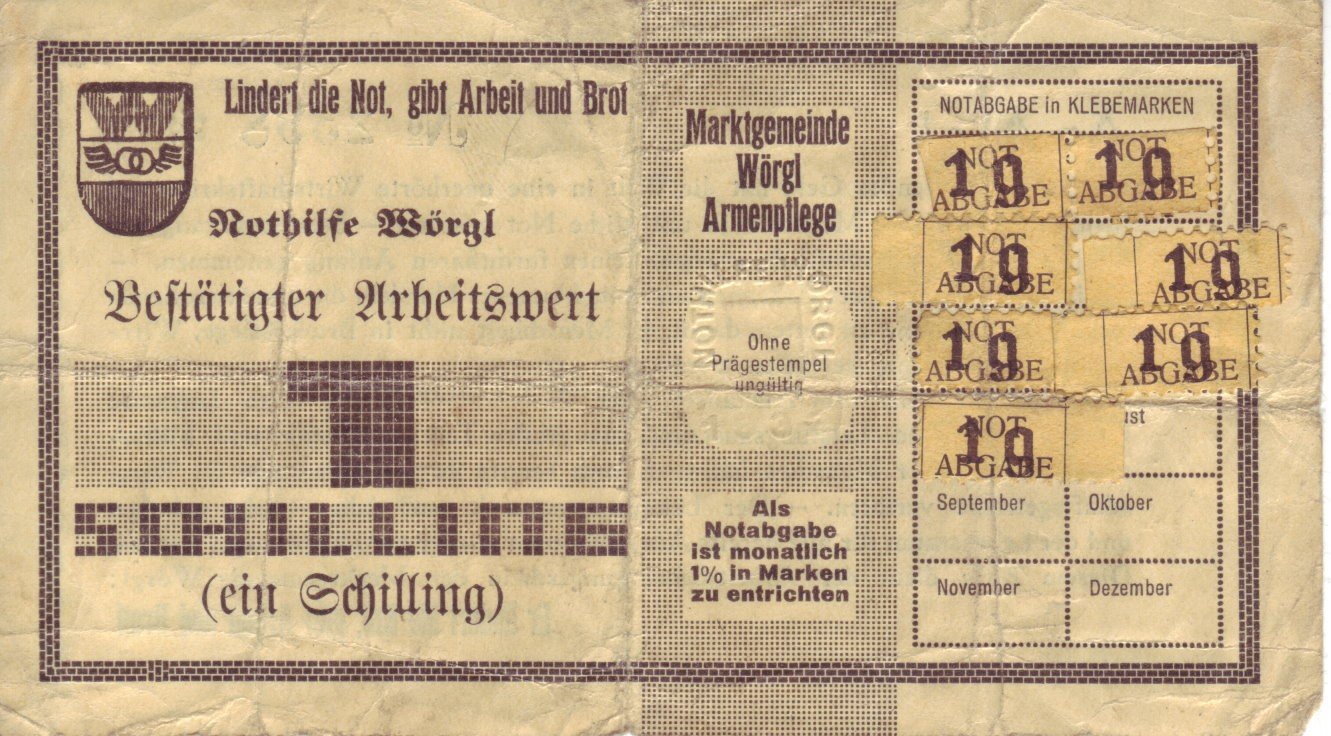

Gesell’s idea regarding money were successfully demonstrated during the depression in Germany but most notably in Wörgl, Austria in 1932-1933. One resident was Michael Unterguggenberger, a railroad engineer who had read Silvio Gesell’s book, The Natural Economic Order, and being excited about the ideas went to the town counsel to propose issuing currency based on Gesell’s ideas, called Stamp Scrip. The counsel was skeptical but desperate to do something because the town had 30% unemployment, there were homeless and hungry families, the town’s factory had closed, and everyone was struggling. So, they elected him mayor. Wörgl, a town of 4500, had 500 jobless people and another 1,000 in the immediate vicinity, and 200 families who were penniless and homeless. The mayor-with-the-long-name (as Professor Irving Fisher, a prominent economist from Yale would call him) having read Silvio Gesell’s work, enthusiastically put it to the test.

The mayor had a long list of projects he wanted to accomplish (re-paving the streets, making the water distribution system available for the entire town, planting trees along the streets and other needed repairs.) Many people were willing and able to do all those things, but he had only 40,000 Austrian schillings in the bank, a pittance compared to what needed to be done.

Instead of spending the 40,000 schillings on starting the first of his long list of projects, he instead put the money on deposit with a local savings bank as a guarantee for issuing Wörgl’s own 40,000 schilling’s worth of stamp scrip. He then used the stamp scrip to pay for his first project. Because a stamp needed to be applied each month (at 1% of face value), everybody who was paid with the stamp scrip made sure he or she was spending it quickly, automatically providing work for others. When people began to run out of ideas of what to spend their stamp scrip on, and seeing the benefits returned to the community so fast, they began paying their taxes in advance.

Wörgl was the first town in Austria which effectively managed to redress the extreme levels of unemployment. They not only re-paved the streets and rebuilt the water system and all the other projects on Mayor Unterguggenberger’s long list, and they also built 200 new houses, ran a soup kitchen feeding over 200 people daily, a ski jump and a bridge with a plaque proudly stating that ‘This bridge was built with our own Free Money’. Six villages in the neighborhood copied the system, one of which built the municipal swimming pool with the proceeds. The French Prime Minister even made a special visit to see firsthand the “Miracle of Wörgl” as did numerous other officials.

Wörgl Stamp Currency

Most of this additional employment was not due directly to the mayor’s projects as was the case, for example, in Roosevelt’s contract work programs. Rather, the bulk of the work was provided by the circulation of the stamp scrip after the first people contracted by the mayor spent it. In fact, every one of the schillings in stamp scrip created between 12 and 14 times more employment than the normal schillings circulating in parallel. The anti-hoarding device proved extremely effective as a spontaneous work-generating device.

In just 15 months Wörgl had accomplished $2.5 million worth of public works while only issuing $6000 due to the high velocity circulation of the currency. It also had a remarkable psychological effect which was that people began to think long term and replanted forest around the town and a bigger water reservoir to provide future capacity. This phenomenon was also true of ancient Egypt, the great pyramids were about the future as were the 1000 great cathedrals and 300,000 churches built by the people across Europe with their own ‘free money.’ Also, women enjoyed more freedom as the Divine Feminine was worshiped, as Isis in Egypt, as the Black Madonna in the High Middle-ages.

Wörgl’s demonstration was so successful that it was replicated, first in the neighboring city of Kirchbichl in January of 1933. In June of that year, Unterguggenberger addressed a meeting with representatives of 170 other towns and villages. Soon afterwards 200 townships in Austria wanted to copy it as did towns in other countries including the U.S. as news of The Miracle of Wörgl spread world-around. U.S. economist Irving Fisher even wrote a book on how to do it, called Stamp Scrip.

It was at that point that the central bank panicked and decided to assert its monopoly authority. The people sued the central bank but lost the case in November 1933. The case went to the Austrian Supreme Court but was lost again. After that it became a criminal offence in Austria to issue “emergency currency.” Many say that this action so angered a large percentage of the population of Austria that they welcomed Adolf Hitler as their economic and political savior.

In our real world today, we have multiple existential crises threatening us, environmental, economic, political, and spiritual. However, most people do not realize that money is the root of these crises, or that money is the governing factor. As economist/ historian/diplomat John Kenneth Galbraith famously said,

“The problem of the modern economy is not a failure of a knowledge of economics; it's a failure of a knowledge of history.” And that “The study of money, above all other fields in economics, is one in which complexity, often a device for claiming sophistication, is used to disguise or to evade truth, not to reveal it. "

There have been proposals to change this, every progressive populist political party in the late 19th century had the issue at the top of their platform, the Chicago Plan in response to the Great Depression caused by the banking system, the 1939 Plan for Monetary Reform, the 2011 NEED Act in response to the 2008 crash, and it is at the bottom of the Green Party’s platform, called Greening the Dollar. All these proposals removed the power of banks to create money and made the government to be the sole issuer of money, all of which was to be spent on the collective welfare. Today most new money goes into the Wall Street speculative economy, benefitting the people who own Congress.

There is a nascent world-around movement to change this system. Some 30 national organizations make up The International Movement for Monetary Reform (IMMR). The American affiliate is the Alliance for Just Money dedicated to educating about and advocating for sovereign monetary reform which should be at the top of our political agenda. We have an exponential monetary economy that is incapable of changing priorities and a linear materials economy that is finite. The monetary reform proposals, such as the NEED Act legislation, seeks to fix that by making labor and materials the limiting factors on money creation. If we don't have the labor and materials to do whatever then no money is created to do whatever. This will help us bring everything back into balance, environmentally, economically, politically and spiritually due to the psychological effects of a positive money system. Anything physically possible, ecologically wise, and socially desirable would be financially feasible.

This legislation would create a public care-motivated system of asset-money that will eliminate debt and begin to heal the damage done by the private profit-motivated system of debt-money. As Frederick Soddy wrote in The Role of Money, creating the money is “the most vital prerogative of democratic self-governance”. It is a political issue because money is the governing factor.

The BRICS Summit

by Mary Sanderson, GPWI

The BRICS summit this week, Aug 22-25 is getting well-deserved media attention. This summary is a comparison of news from social media, US legacy and financial, and quotes from BRICS spokespersons.

Social media are building suspense on two things: a supposed release of “BRICS coin”, possibly backed by gold and the imminent, chaotic collapse of the dollar as world reserve currency. The coin rumor is typical gold dealer sales pitch. The slow-motion collapse of the dollar is real. We are living it in the form of social and environmental crises.

BRICS spokespersons have said there is no coin any time soon. BRICS’ stated goal is to support and promote countries’ settling trades among themselves using their own national currencies. That is clearly a response, and a threat, to abuses of dollar hegemony. International trade settlements in other monies are beginning. China already buys some of its oil with yuan.

As the US increasingly weaponizes financial sanctions (freezing funds of non-compliant countries) the BRICS proposal looks increasingly attractive to the vulnerable, and this year suddenly 23 countries are applying to join, including Saudi Arabia.

The legacy press and the financial press reporting this week’s BRICS summit are making Saudi Arabia’s sooner-or-later admission the big deal. Because Saudi Arabia’s longstanding agreement to accept only dollars for oil has been the lynchpin of dollar primacy (1971 until recently) there is wild speculation about how fast BRICS with the Saudis could crash the whole world economy. It rests on the assumption that all world leaders are as corrupt as the Europeans and Americans.

BRICS spokespersons are excited to announce agreements on protocols, deliberate criteria for accepting new members. This leads to two more stories in US media regarding the summit: one is the argument that China is in a hurry to build a BRICS block against NATO. That is great for building anti-China sentiment here in the US. The other story is hoping for a rift between China and India who supposedly wants to build BRICS more slowly to leverage concessions from the power centers over time.

BRICS definitely merits our attention. It provides good exercise in finding truth across media sources and between the lines.

Declared by the Institute of International Finance “The illusion of limitless fiscal space has ended abruptly in recent months."

The Most Important History is the History We Don't Know

Robert De Fremery

by Howard Switzer, GPTN

For five decades, Robert De Fremery was one of the most consistent forces for monetary reform in America. Though not generally known to the public, De Fremery’s persistent correspondence with Federal Reserve authorities, and nationally known economists has had a lasting influence upon many of them. His ideas on one hundred percent reserve banking and increasing the money supply in proportion to population growth, have appeared over the years in prestigious financial journals, as well as in his previous book MONEY AND FREEDOM.

De Fremery’s lifelong concern has been how the rights of all Americans have been sacrificed in the name of awarding two special privileges to a tiny minority. These two privileges are the specially favorable tax treatment of landholders and the monetary powers of bankers.

Equal rights for all, special privileges for none.

In his book RIGHTS VS. PRIVILEGES, he elegantly and simply presents “An analysis of these two powerful privileged interests that have deprived us of fundamental rights.”

MONEY CREATION A GOVERNMENT PREROGATIVE

As I see it the only reason (and I do not consider it a valid reason) for allowing banks to borrow short to lend long is that it makes possible an expansion of ‘the supply of money’. But this is not a proper function of the banking system.

Creating money must be divorced from the lending of money. The power to create money must be confined to governments alone and limited by constitutional safeguards. Banks must not be allowed to lend their credit, but only money placed with them for that purpose…The existing value of bank credit, which is being used as money, will have to be monetized and completely divorced from gold.

Our current monetary system is institutionalized usury.

Usury:

The abuse of monetary authority for personal gain.

The great religions and philosophers condemned usury.

Dante described it as

An extraordinarily efficient form of violence by which one does the most damage with the least amount of effort.