Any government that does not control its money is controlled by those who do.

Money is POWER

By Rita Jacobs; Published 5/10/20, by Green Party of Michigan

The greater the power the more dangerous the abuse.

— Edmund Burke

The word cloud that accompanies this article was created in an online course when the students were asked to enter three words that came to mind when they thought of money. Yes, money is power. The pursuit of money is necessary for most of us at least to provide ordinary living necessities. However, for some in our society the pursuit of money becomes an end in itself, fueled by greed for both money and power.

This MIT course, Just Money, that created the word cloud, described a number of community banks and credit unions in various countries that were established to partner with and help small communities where many of the small businesses had no “customer” relationship with larger banks. Many of the small banks, besides having a goal to help the communities, also had goals to direct their loans to those businesses that promoted eco-friendly practices while providing needed services to the community. And to its credit, MIT included in one segment of this course an explanation of how banks also have the power to create money. The object of the course was to illustrate how a bank can contribute in positive ways to put the needs of communities ahead of its profits.

Unfortunately, many community banks may not be much help to small businesses post-pandemic. We already know that the initial stimulus package passed by Congress contained measures that were allegedly for assistance to small businesses through loans that could be forgiven if they were used to pay the wages of their employees. We already know what happened to those loans. Most of them went through big banks to those who least needed the loans, leaving little for family owned smaller businesses. It is apparent that the government has no idea how to provide help to small businesses in this kind of crisis. This is no surprise when the government ignores the needs of most people, and enacts laws that favor the elite.

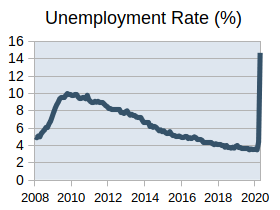

In 2018, Congress passed the Economic Growth, Regulatory Relief, and Consumer Protection Act (EGRRCPA) that resulted in a comprehensive deregulation of community banks. The CARES Act provided a waiver of additional banking regulations affecting community banks. This will allow community banks to make somewhat riskier loans than before. Some experts think this deregulation of community banks is a very bad idea. As of the first week in May, more than 33 million Americans had filed for initial unemployment benefits. Predictions for the near future are waves of defaults on loans that will create conditions for a major depression in the economy. So, is this a proper climate for community banks to take on riskier loans? Probably not.

Looking back at bank failures after the crash of 2008 may give us some idea of what to expect. There were 489 bank failures from 2008 through 2013. All but 9 were community banks. A “bank failure” is the closing of a bank by federal or state regulators, with the Federal Deposit Insurance Corporation (FDIC) covering insured deposits. According to the FDIC, more than $47 billion in federal funds were spent in the process of resolving the 480 community banks that failed. Post-pandemic, we are probably looking at another significant wave of community bank failures.

Each time there is an economic crisis of some sort, there is a shift in wealth, creating greater wealth disparity. There is no reason to expect anything different resulting from the pandemic. In 2018 the Federal Reserve System identified 12 “too-big-to-fail” banks that could threaten the stability of the U.S. financial system. The big banks have continued to increase their wealth since the crash in 2008. We are seeing the start of another bailout of big banks and corporations. These financial institutions have as their main goal increasing their own wealth. Their disregard for people and the planet is apparent when they use their immense wealth to control the government by financially backing the legislators who will enact policies that protect their wealth creation.

The 99% cannot continue to bear the burden of financial loss under this current monetary system. The rate of poverty and homelessness cannot continue to climb while a small number of wealthy oligarchs continue to grow their excessive fortunes.

It is most important now to spread knowledge about the monetary system, and how it contributes significantly to the present wealth disparity. Capitalism is not the sole culprit. There is no reason why the government should allow banks to create money that is loaned back to the government with interest. Nor is there any good reason to allow banks to create money and loan it to favored corporations in order to increase the value of their own stock in the same corporations, while receiving interest payments on their loan. Banks should not be given this special privilege that has allowed them to accumulate unchecked wealth and power. And no bank should be too big to fail.

The solution is not to ‘reform’ our debt-based money system, but to replace it with a system where money is created debt-free.

Why Collapse?

By Kevin McCormick — Green Party of Texas

The covid-19 pandemic has forced a new focus in our thoughts. We begin to ask why the world is the way it is. The United States is attempting to return to “normal” activity which brings the likelihood of the pandemic worsening to new levels of crisis. But our leadership feels compelled to attempt this quixotic charge in a desperate effort to save the system.

Why do we live in a social and economic system that can only exist in a state of frantic movement forward and up, and for which it is impossible to pause for a while?

Yes, we are currently facing a serious epidemiological problem, but all the ensuing social and economic problems are self-inflicted and there is absolutely no rational reason for them to develop. The economy is going collapse because it is based on a giant hyper-complex and ever-expanding tangled mess of leveraged debt relationships that will implode when rent and mortgage payments are no longer made.

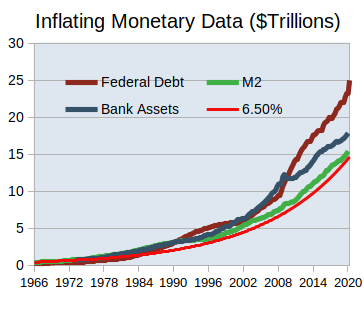

The financial system must inflate exponentially to enable the debtor-creditor relationships to function. Inflation makes compound interest possible by increasing banking cartel debt and money at an average rate of about 6.5% annually. Since the creation of the Federal Reserve in 1913, the dollar has been inflated by approximately 26 times and is now worth less than 4 cents. Under the Federal Reserve the U.S. monetary system has been given over to an elite who employ bank-created deposit money as a means to acquire profits. This money is created by accounting entries to fund loans made by banks and profits are derived from interest paid by the borrower. In fact, it is a system of institutionalized usury.

Interest payments are the primary source of profit under this banking-cartel monetary system. This is shown by corporations making profits from financing customer purchases rather than from their business operations. The wealthy collect far more interest than they pay out. Income Inequality in the Unites States, 1913-2002 The mathematical fact is exponential inflation of debt and money is necessary to enable the debtors to make payments and the creditors to derive profits.

The pandemic has undermined the Federal Reserve System by removing its ability to sustain monetary inflation. With 33 million new unemployment claims and an estimated GDP decline of 30%, banking cartel money creation through lending will virtually cease. This economic decline will eliminate profitable lending opportunities and will pull the rug from under the debt-money system. Yet, paradoxically, monetary statistics show an increase in the money supply. Both M1 (demand deposits and currency) and M2 (money market funds and time deposits added to M1) have increased sharply in March and April. Federal Reserve Bank credit (loans to banks and assets acquired from banks) has exploded to $6.5 Trillion. The propaganda message may be about the upcoming recovery, but Federal Reserve actions show they see a coming tsunami of loan defaults and bankruptcies.

While the U.S. government and the Federal Reserve are rushing to support the upper strata of the financial hierarchy, ordinary people are being left to make do however they can. The aid will help support the establishment, but it will not do much to circulate money to working people. It certainly will not alleviate hopelessness and despair. With collapsing GDP and exploding unemployment, it seems likely that an enduring economic depression is unfolding.

Against the economic drop, the CARES Act allocates a total of $2.2 trillion. It is funded by the federal debt which has increased to $23 Trillion. The headline numbers are large, but the effective circulation is likely small. Much of the CARES Act funding is in the form of loan guarantees, while direct payments will do little to relieve economic insecurity. In an economy that has seen its money creation machine throttled down to a stall, the CARES Act is poorly designed and inadequate.

Due to the covid-19 pandemic, the curtain has been pulled back from the Federal Reserve monetary system. The sight of privileged corporate aristocrats juxtaposed with despairing working families is not a pretty one.

We are sorely tempted to blame this mismanagement and neglect on the government, but it would be more accurate to blame the lack of government. The Federal Reserve system in the United States is based on the absence of Congress exercising its constitutional power to “coin money and regulate the value thereof.” The U.S. Congress is perhaps more despised today than ever before in its history. The reason is clear—Congress has failed to exercise its powers to serve the public and has allowed a predatory banking cartel to have control over the national economy.

Instead of rushing to restore a broken and unsustainable system, and continuing social injustice and environmental destruction, we can take this opportunity to transform our society to achieve the goals of sustainability, social justice, and economic security which so many people share. The Green Party platform advocates far-reaching monetary reform, including the creation of debt-free money, removal of money creation ability from private interests, universal basic income, and a fair and beneficial distribution of money in our society. This is the best time we have had in our lifetimes to challenge the ruling establishment and achieve reform. The Green Party monetary reform measures give us a solid foundation to transform the monetary system into something that serves the public interest. It is time to enact these reforms.

The Government should create, issue, and circulate all the currency and credits needed to satisfy the spending power of the Government and the buying power of consumers. By the adoption of these principles, the taxpayers will be saved immense sums of interest. Money will cease to be master and become the servant of humanity.

'Planet of the Humans': Toward a Greener Green

By Howard Switzer — Published 5/7/20 on Medium.com

Jeff Gibbs Planet of the Humans is a powerful film I think because it exposes the reason WHY we have to change the way we live on this planet, and do it now because we’re at the end of the fossil fuel era. Thanks to Michael Moore it has been broadly available for people to see. The film shows how industrial capitalism, despite using renewable energy technologies, solar, wind and biomass, continues to devastate life on this planet. It is not new information but the backlash from the left and some environmentalists exposes an unhealthy attachment to a techno-fix. It shows how the big financial interests have funded non-profit environmental groups in order to perpetuate the fraud that renewable energy technologies can power industrial civilization. The elite have long known that funding the opposition gives them control of the opposition. While the film identifies population growth as a problem it reveals that it is our extreme level of consumption that is the bigger problem. Unfortunately the film stops short of exploring a solution only that we must use and live on less, something that fits with the capitalist imposition of austerity on us while they flaunt their yachts.

I hope Moore will now do a film that exposes the myths about money, one that will delve into the mechanics of Capitalism, which is the private control of the creation and allocation of what we use for money. Using credit/debt for money systematically concentrates wealth to the wealthiest who often use it to control public policy in their favor, undermining good economic, social and environmental policy. Because all our money is created by the private for-profit banking industry, owned by the oligarchy, it allows them to direct the entire economic development of society.

It has been sufficiently proven that such power in the hands of a few elites means very bad public policy decisions. After all, how many can resist such power to improve their own position over everyone else? Money is the most influential of all man-made systems and is much more about power than it is economics. This is why the power to create it should not be in a few private profit-motivated hands but in broadly represented and accountable public hands originating and allocating money for public purpose. The population has been dumbed down by the schools and media that comprise the elite’s social management system perpetuating the myths.

Myth number one: the government creates and issues all our money. This is exactly how everyone knows it should be, it’s in our Constitution and it was recognized throughout history all the way back to the ancient Greeks 10 centuries before Christ that the creation of money was the most vital prerogative of democratic self-governance. US history is full of the monetary issue, the American Revolution was fought over the issue of creating money and publicly issued money (Continentals) funded the revolution. Publicly issued money (Greenbacks) saved the Union during the Civil War and publicly created and allocated money would have ended the depression in one month if Henry Simons, Paul Douglas, Irving Fisher and a couple hundred other economists’ recommendations had been heeded in the 30s. However, the banking system has dominated monetary policy and the issuance of money from the very beginning when Hamilton, our first Treasurer, ‘convinced’ Congress to hand over the nation’s monetary authority to The First Bank of the United States owned by his friend and future partner, Robert Morris.

Myth number two: the banks lend out deposits of existing money. This never happens; banks create money by typing numbers into an account at the instance of a loan and extinguish it as the loan is paid off. Since the money created is just the principal, the interest must be acquired from the principal of another’s loan. This creates a highly competitive economy that systematically concentrates wealth to the wealthiest. Americans are ignorant of the money system because it is not taught in schools at any level, even the university level. These false assumptions are why economists are unable to predict much at all regarding the economy. As the great economist, John Kenneth Galbraith said,

The problem of the modern economy is not a failure of a knowledge of economics; it’s a failure of a knowledge of history. . . . The study of money, above all other fields in economics, is one in which complexity is used to disguise truth or to evade truth, not to reveal it. . . . The process by which banks create money is so simple that the mind is repelled. . . . The solution is not to“reform” our debt-based money system, but to replace it with a system where money is created debt-free.

A friend of mine says “Public money won’t fix everything but it makes everything fixable.” It would be so great to explore a vision of a transformation from the current ‘economics of greed’ into an ‘economics of care’ funded by a Public Money System. The pandemic has exposed the injustice and greed of our money system as well as how fast the air and water clears when we stop what we’re doing. We can rebuild the local economies destroyed by capitalism and localize food production on a massive scale. We can build community scale food, fuel and power systems where the waste of one system is the feed-stock for the next, closing the waste loops. Only a public money system is capable of making that kind of public investment. Instead of wealth flowing to the few at the center, money would flow out to the many. This is because it is not money issued as debt, it is money issued as money, a permanently circulating public asset, based on a share in our national equity and spent or gifted into the economy for the general welfare.

In fact the legislation is already written and was introduced to the 112th Congress, The NEED Act HR 2990. It would fund healthcare, education, a 21st century food, energy and transportation infrastructure without incurring debt and interest payments. It calls for 25% of new money to go to the states on a per capita basis and a $10,000 citizen’s dividend to fill the gap until government spending is ramped up. It would shrink the elite’s speculative Wall Street economy and boost the people’s productive economy creating a steady-state economics of care. The story of money is the story of power, and I find it vexing that it has been left completely out of our education.

Fortunately the information at long last is getting out on the Internet, books and articles. There are individuals, like Joseph Huber, Virginia Hammon, Mari Werner, and others as well as organizations like Alliance for Just Money and American Monetary Institute, educating people about money, and the International Movement for Monetary Reform, is a growing coalition of 30 some monetary reform groups around the world. The Green Party is the only political party that includes monetary reform in its platform and the elites, as always, are funding efforts to confuse and derail any talk of monetary reform.

The wealthy fear democracy, I get it. That is why it is important to show democracy as non-threatening, there is plenty to go around. A private for-profit debt system (plutocracy) generates scarcity and fear, a public asset system (democracy) generates abundance and care. Money has psychological consequences we should all be aware of. It is apocalypse now and the veil is lifting exposing the crimes of the elite hearkening the end of the current system and a new beginning. As Tom Paine said, and it is still true: We have the power to begin the world over again.

The institutions that create and distribute money in our nation and throughout much of the world are diseased.

Monetary systems are supposed to ensure that economies are healthy, just and sustainable. They shouldn't benefit the 1% at the expense of the rest of us.

The COVID-19 pandemic has exposed and worsened the inherent crises in our medical and economic system. The same is true of our monetary system, which in its own right is as invisible, harmful and widespread as the virus, but was unjust, unsustainable and undemocratic long before the first cough, sneeze, or breath from a coronavirus-infected person occurred on US shores.

The Federal Reserve System, our nation's central bank, composed of 12 Regional Reserve Banks, creates money out of thin air -- as do all commercial banks across the country.

The Fed will be issuing money in the current crises by literally entering numbers in bank accounts of some corporations as loans and to other corporations to purchase assets, mainly corporate bonds. The Fed will create the money and decide the major corporate recipients of the trillions. It will also dole out an additional several hundred billion dollars from the government's recent stimulus bill to large corporations.

A return to economic “normalcy” post COVID-19 won't happen and shouldn't be our goal. Now is the time to organize for economic and political systemic change, including a democratized money system that will serve the interests of people and communities over those of Wall Street and other financial interests.

The U.S. Constitution (Art 1, Sec 8) authorizes Congress to “coin” (a verb) money. Money creation, along with spending and taxes, are the three major economic tools of the federal government. Federal spending and tax policies (which receives the most public attention) repeatedly favor the super rich and corporations - including the several trillion dollars worth of bills recently passed by Congress. Monetary policies are different. They not only favor the rich and corporations. The corporations are the decision-makers.

Without a shot being fired or tanks rolling into the nation's capital, corporate interests pulled off a financial corporate coup with passage of the 1913 Federal Reserve Act - capping a century long struggle between banksters and the public over who (or what) should have the right to have their hand on our nation's money spigot. Previous efforts to privatize/corporatize money creation were beaten back when both the corporate charters of the private First National Bank (1811) and Second National Bank (1836) weren't renewed.

The Federal Reserve System is largely a private/corporate network - more beholden historically to its Regional Banks and their banking corporation members than to the public.

All new money in our nation, minus coins, is created by banks out of thin air with only a small percentage, if any, of deposits to back them up. Most of the new money is interest-bearing loans for homes, vehicles, business creation/expansion, etc., which is debt. New money is also used to buy Treasury bonds and other securities, which is also debt.

Let this sink in. Congress can only literally nickel and dime the issue of money creation. Our government currently cannot create money as an asset - unable to use one of its three constitutional financial tools to respond to our unprecedented economic crisis that is decimating individuals, small business, local and state governments, and the larger economy. The creation and distribution of money by banks is the most economic and democratically damaging form of privatization/corporatization in our society.

Robert Hemphill, former Credit Manager of the Federal Reserve Bank of Atlanta, chillingly described decades ago this reality:

We are completely dependent on the commercial Banks. Someone has to borrow every dollar we have in circulation, cash or credit. If the Banks create ample synthetic money we are prosperous; if not, we starve. We are absolutely without a permanent money system. When one gets a complete grasp of the picture, the tragic absurdity of our hopeless position is almost incredible, but there it is. It is the most important subject intelligent persons can investigate and reflect upon. It is so important that our present civilization may collapse unless it becomes widely understood and the defects remedied very soon.

Banks' legal authority to create money as debt led to loans for speculative stock investments in the 1920s, the subsequent stock market crash and the Great Depression. It resulted in bank lending for risky mortgages in the late 1980s that banks mixed together, what they called “securitized,” with AAA ratings and sold off to unsuspecting investors that eventually crashed - causing massive losses of money and homes, but also billions for bank bailouts during the Great Recession. Senator Dick Durbin's refreshingly honest observation explained the reason for the bank bailouts: “And the banks -- hard to believe in a time when we’re facing a banking crisis that many of the banks created -- are still the most powerful lobby on Capitol Hill. And they frankly own the place.”

A financial reckoning was imminent before COVID-19 – in no small measure due to the Fed's power to create money as debt. Its persistent low interest rates allowed corporations to borrow money cheaply — not to expand research & development or to raise worker salaries to increase benefits, but for stock buybacks to pump up share prices. This increased payouts to CEOs with compensation packages that included equities. It also drove up the stock market and further widened the rich-poor gap since the rich disproportionately own stocks. Wall Street’s health, though, didn't reflect the growing sickness of main street or the side or back streets of our economy.

The Fed has injected more than $9 trillion in short term loans, called “repo loans,” to Wall Street to keep the interbank loan market from collapsing since last September. This propped up and concealed at least one “too big to fail” bank from default.

The recently passed CARES Act included $454 billion for the Treasury Department earmarked to the Fed to help big businesses. The Fed leveraged the amount ten times to create over $4 trillion in loans to banks and other corporations. Just recently, the Fed expanded the program to include even larger businesses with even more debt due to the coronavirus. Who receives the cash will be decided by private banks, not our government -- despite the $454 billion being public funds. Some, if not all, of the nearly half-trillion dollars will be spent buying bad investments (also known as “junk bonds”) from banks and other corporations, which incentivize risky investments when you know you’ll always be bailed out for bad bets.

Just to make it as difficult as possible to, if nothing else, shame banks into acting at least somewhat publicly accountable, the Fed has not committed to disclosing the bank recipients of the $9 trillion in repo loans. Moreover, the CARES Act suspends the Freedom of Information Act for the Fed and allows it to hold secret meetings on corporate bailouts with no publicly-released minutes. Further evidence that banking corporations rule.

At some point, of course, the bills will come due. The public will be on the hook to pay at least the interest on a $27 trillion or larger national debt by year’s end. This will consume an even larger share of our federal budget. We all know what that means.Without money creation in our public/democratic financial tool kit, we're left with just spending and taxes. The perennial debate will commence over whether to slash social programs (which will include entitlement programs like Social Security and Medicare, as well as programs that help those in our nation most in need) promoted by Republican vs raising taxes on the super rich and corporations (and maybe, just maybe, even puny military spending cuts) offered by Democrats. The truth is both parties can slash and tax away, but it still won't come close to taking a real bite out of the debt. Selling or leasing every public asset or service to corporations will be debated. Economic Einsteins will also suggest addressing the debt problem by simply borrowing more -- analogous to the belief that you can drink yourself sober.

Being in debt means being in servitude to those who own the debt. Most of us work a large part of the year to pay banks mortgages, credit cards, student loans, auto loans and other debts. In the case of the federal government, debt takes the form of Treasury bonds - which right now are owned by the Fed, but also by banks, mutual funds and pension funds. More than one quarter of US debt, however, is owned by foreign nations, with the major holders being China, Japan, Brazil and the UK. These countries at some point might come calling to pay up. If we don't have the cash or the dollar is deemed worthless due to all the money printing, then it may be our national parks, forests of other physical assets that are handed over to the countries or their national-based corporations. It's what the US-dominated IMF and World Bank have done for decades toward other countries as “conditions” for loans.

A “sovereign or just money“ system is the alternative to our socially, economically and politically diseased bank-created money system. Public creation of money must go beyond minting coins. It happened before when the Lincoln administration issued debt-free “Greenbacks” to finance the Civil War. A democratic money system must also include ending the ability of banks to create money as interest-bearing debt.

Such a system doesn't have to be created from scratch. The National Emergency Employment Defense (NEED) Act was introduced in several Congressional sessions, most recently in 2011 by former Congressman Dennis Kucinich and the late John Conyers.

The NEED Act would create public money as an asset. It would gradually eliminate our federal debt, spend public money to meet a variety of human and physical infrastructure needs creating millions of jobs, provide funding to state and local governments, and even provide a “citizens dividend,” along with many other provisions. Since newly created U.S. money would be spent on real goods and services, there would be no inflation, as economic/mathematical analysis concluded. Additionally, banking corporations could no longer create money out of thin air as debt by computer keystrokes.

The beauty of the Act is that its transformative proposal accomplishes what most of the public believe already exists. Thanks to Wall Street, their media mouthpieces and economic cheerleaders, we've all been conditioned to accept these three monetary facts:

The Federal Reserve is public

The U.S. government creates all of our money

Banks only lend what they have in reserve

Reality for more than a century has been just the opposite. The NEED Act is monetary jiu jitsu. Its major transformative provisions are precisely what we've been led to believe has existed all along. It’s extremely rare that any profound proposed systemic change is based on core elements already widely perceived as the truth by the public. Thank you very much Wall Street banksters and your sycophants!

The NEED Act needs updating. The Alliance for Just Money is circulating a petition calling for the Establishment of a National Commission of Inquiry Into the Money System of the US to deal with the issue proactively. We can't wait until economic conditions further deteriorate and banking corporations gain ever more profits and power.

The NEED Act, Medicare for All, national paid sick leave and unemployment insurance are among several policies that the current COVID-19 and economic crises have exposed as being urgently needed. Enactment of any of them is extremely difficult in a politically rigged system dominated by the super rich and corporate entities.

Banking corporations are among the most politically potent. The Finance, Insurance and Real Estate (FIRE) industry continues to be #1 in political campaign contributions/investments in the current election cycle, as it has been for many years. Seats on the House Finance Service Committee are among the most coveted since the financial industry rains campaign contributions down on its members, which has increased in size to 61 from 44 members since 1980.

Canadian Economist William Hixson summed up the societal challenge of creating a democratic money system:

The very idea of a government that can create money for itself, allowing banks to create money that the government then borrows, and pays interest on, is so preposterous that it staggers the imagination. Either everyone in government in charge of the procedure is lacking in intelligence or they have been bought and paid for by those who profit from their skullduggery and their infidelity to the public interest.

It may be that none of these needed changes occur until all of their respective advocates come together in a larger movement of movements. Included in this should also be Move to Amend's We the People Amendment to the US Constitution to abolish corporate constitutional rights and declare that political money in elections is free speech — a solution that would make it easier to achieve all of these and other separate social and economic ills.

The challenges are immense. The crises are enormous. Our solutions must be equivalent in scale.

COVID-19 looks to be the pin that has popped the “Everything Bubble” financially, opening the possibility for a reset of our economy, as well as our governing institutions and social order to be more authentically democratic, decentralized, just and sustainable. Promoting half-measures is comparable to premature ending of stay at home orders to flatten the coronavirus curve. The problems and virus will simply continue.

Fundamental system change is the only approach to curing our monetary pandemic and other structural diseases.